BY: Matthew Kimbrough

Portfolio Manager

Leading up to Today’s Decision

While it was not quite unfathomable that the first Fed Funds rate cut in this monetary policy cycle could occur today, it would have nevertheless been an extremely unlikely outcome. Expectations were firmly in place for the Fed Funds rate to remain unchanged after this month’s FOMC meeting.

Six weeks ago, the Statement that was released after the January FOMC meeting specified that the Fed required “greater confidence” in inflation prior to instituting any rate cuts. However, economic data on inflation has been stronger instead of weaker over the past two months – so much so that the Fed likely has less confidence that inflation is falling meaningfully back towards their 2% target. Still, market participants have been left wondering what “greater confidence” really entails and whether this threshold can be quantified by the Fed.

Today all eyes will be on the new Statement of Economic Projections (SEP) and on Powell’s press conference. Last time around, we were also told that there would be in-depth discussions of the Fed’s balance sheet at this meeting. Specifically, there are questions about the pace of balance sheet runoff (QT) and whether this pace will need to be moderated soon, as the optimal balance sheet size is approached. The only problem is that nobody knows for sure what the optimal size of the balance sheet actually is, or precisely how the Fed makes this determination. Hopefully, we will get more clarity about this process. One thing we will definitely receive is an update to the SEP, complete with a new Dot Plot and projections for growth, unemployment, and inflation.

The Decision

The Fed Funds rate remains unchanged. It has been held at its present range of 5.25 – 5.50% since the July 2023 FOMC meeting.

The Statement

Last meeting’s Statement contained some key amendments (including the removal of the Fed’s bias toward tighter monetary policy and the requirement for greater confidence in inflation) but the changes to this month’s Statement were much less noteworthy. Only the second sentence was amended, retaining language that “job gains have remained strong,” but removing the reference to gains moderating since early last year.

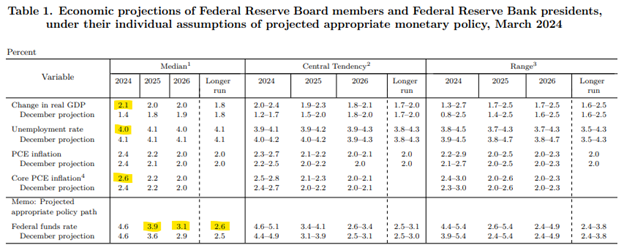

New Economic Projections

The most significant changes to (or facets of) this quarter’s Statement of Economic Projections (SEP) document have been highlighted below:

1. The median Dot Plot projection remains the same – three 25bp rate cuts are projected in 2024

2. The number of expected rate cuts in 2025 fell from four to three

3. The long-run Fed Funds target rate increased from 2.5% to 2.6%

4. GDP was revised up significantly, from 1.4% to 2.1% in 2024

5. Unemployment projections fell to 4.0% for this year from 4.1%

6. Core PCE inflation expectations rose 0.2% to 2.6% in 2024

The Press Conference

The Fed’s balance sheet holdings will continue to be reduced as previously described, but Powell elaborated in his prepared comments before the press conference by stating that, “Our securities holdings have declined by nearly $1.5Trillion since the committee began reducing our portfolio. At this meeting we discussed slowing the pace of decline of our securities holdings. While we did not make any decisions today on this, the general sense of the committee is that it will be appropriate to slow the pace of runoff fairly soon, consistent with the plans we previously issued. The decision to slow the pace of runoff does not mean that our balance sheet will ultimately shrink by less than it would otherwise, but rather it allows us to approach that ultimate level more gradually. In particular, slowing the pace of runoff will help ensure a smooth transition, reducing the possibility that money markets experience stress, and thereby facilitating the ongoing decline in our securities holdings consistent with reaching the appropriate level of ample reserves.”

Another interesting statement within Powell’s opening remarks was that “an unexpected weakening in the labor market could also warrant a policy response.”

In the press conference, when asked about whether recent inflation data had dented FOMC member’s confidence levels, Powell replied, “It certainly hasn’t improved anyone’s confidence. But the story is the same – inflation is coming down towards 2% on a somewhat bumpy path.” There were several instances where he referred to potential seasonal effects within Q1 inflation data. However, he also stated, “You have to be careful about dismissing parts of the data that you don’t like… We don’t really know yet whether this is a bump in the road or something more.”

The Market Reaction

2-year Treasury yields rallied around 6bp during the Fed’s press conference, while the 10-year Treasury yield declined by just 1-2bp. Equity markets continued to rally.

Not Investment Advice or an Offer | This information is intended to assist investors. The information does not constitute investment advice or an offer to invest or to provide management services. It is not our intention to state, indicate, or imply in any manner that current or past results are indicative of future results or expectations. As with all investments, there are associated risks and you could lose money investing.